Market Review - Third Quarter 2024

Stocks delivered impressive returns in the third quarter of 2024. While large U.S. companies continued to perform strongly, smaller companies began to outpace them. Foreign companies (which have lagged behind large U.S. companies) enjoyed a boost following European Central Bank (ECB) rate cuts and easing concerns of a recession. The quarter was marked by moderate economic growth, easing inflation, declining interest rates, and rising corporate profits. However, uncertainties related to conflicts in the Middle East and Ukraine, the upcoming presidential election, and the Federal Reserve’s ability to balance policy objectives of full employment and price stability, continued to linger.

Equity Performance for Periods Ending on September 30, 2024

| Total Return Index | Market Sector | Quarter | YTD | 1-year | 3-year | 5-year | 10-year |

|---|---|---|---|---|---|---|---|

| S&P 500 | Large U.S. Companies | 5.9% | 22.1% | 36.4% | 11.9% | 16.0% | 13.4% |

| Russell 2000 | Small U.S. Companies | 9.3% | 11.2% | 26.8% | 1.8% | 9.4% | 8.8% |

| MSCI EAFE | Developed Int’l Markets | 7.3% | 13.0% | 24.8% | 5.5% | 8.2% | 5.7% |

| MSCI EM | Emerging Int’l Markets | 8.7% | 16.9% | 26.1% | 0.4% | 5.8% | 4.0% |

| BB US Agg Bond | US Investment Grd Bonds | 5.2% | 4.4% | 11.6% | -1.4% | 0.3% | 1.8% |

The final reading on U.S. real GDP for the second quarter of 2024 indicated a 3.0% annual growth rate. However, the economy faces challenges such as high consumer debt, elevated interest rates, and weak consumer confidence. Despite a decline in the Conference Board Leading Economic Index for six consecutive months, a recession in the near term is deemed unlikely by most economists. The Conference Board projects overall growth of 2.4% for 2024—slightly above the Federal Reserve’s estimate of 2.0%. Most estimates for 2025 suggest economic growth will be around 2%.

Inflation continued to decline during the quarter, with the Consumer Price Index dropping to 2.5% in August, its lowest level since February 2021. As inflation concerns eased and unemployment rose slightly, the Federal Reserve cut its benchmark interest rate by 0.5% in September, bringing it to a range of 4.75% to 5.00%. While the market anticipated a rate cut, most investors welcomed the 0.5% decrease. Further cuts are expected, as indicated by trading in Fed Funds futures which suggest the rate will fall to 2.8% by the end of 2025.

Lower interest rates tend to stimulate the economy, encouraging purchases by both consumers and businesses as borrowing costs decrease. What is particularly encouraging for the market is that interest rates are declining while the economy continues to grow. In many previous interest rate cycles, the Federal Reserve waited to cut rates until a recession was imminent.

In the week after the Federal Reserve’s interest rate cut five other central banks made rate reductions. China, the world’s second-largest economy, introduced other measures to stimulate its economy and boost its stock market. These actions helped drive strong performance in international investments, as well as for U.S. companies that generate a substantial share of their revenue from global markets.

According to FactSet Research, earnings for companies in the S&P 500 are projected to grow by 4.6% in the third quarter of 2024, marking the fifth consecutive quarter of year-over-year growth. The estimates for earnings growth for all of 2024 and 2025 are 10.0% and 15.2%, respectively. A number of sectors that were hurt by higher interest rates in 2024, especially those tied to consumer spending, are expected to perform better as rates decline.

On a valuation basis—using metrics such as price-to-earnings (P/E) ratio—the S&P 500 Index appears to be expensive compared to historical averages. Investors are generally willing to pay a higher price for earnings that grow consistently. According to FactSet, the S&P 500 currently is trading at a forward P/E ratio of 21.4, considerably higher than the five and 10-year averages of 19.5 and 18.0, respectively. However, as we have noted in several past letters, the valuation of this index is skewed by a few technology companies whose stock prices have benefited from exuberance related to artificial intelligence (AI).

The S&P 500 Index is weighted by the market value of its 500 constituent companies. Currently, the largest ten companies represent 36.2% of the index’s total value. Seven of those companies are large technology companies collectively called the “Magnificent Seven” AI firms. These top 10 companies have an average price-to-earnings (P/E) ratio of 33.5, compared to the remaining 490 companies, which trade at a more modest P/E ratio of 17.2. As shown in the following table, most sectors of the equity market appear reasonably valued. While the portfolios we manage have exposure to these top ten companies, we believe maintaining a high degree of diversification mitigates the risk associated with potential overvaluation from AI-driven speculation. Although we expect AI to play a significant role in shaping businesses and the economy, we believe its benefits will extend well beyond the largest ten U.S. companies. Furthermore, we are skeptical that the vast resources being spent in pursuit of AI breakthroughs will ultimately deliver the returns needed to justify the current valuations.

Forward P/E of Index Components

| Index or Components | Forward P/E |

|---|---|

| S&P 500 Index | 21.4 |

| S&P 500 largest 10 Companies | 33.5 |

| S&P 500 next 490 Companies | 17.2 |

| S&P 500 Equally Weighted Index | 18.3 |

| S&P 400 Mid Cap Index | 17.5 |

| S&P 600 Small Cap Index | 16.1 |

| MSCI EAFE Index (developed international markets) | 14.5 |

| MSCI EM Index (emerging international markets) | 13.2 |

Historically, stock market corrections have rarely been attributed solely to overvaluation. However, when a correction does occur, there is more potential downside for companies with excessive valuations.

Major conflicts in the Middle East and Ukraine have caused immense pain and suffering for millions in those regions, resulting in countless deaths and widespread humanitarian crises. These wars have severely disrupted supply chains for vital resources, including oil, natural gas, grains, fertilizers, and key metals, while also prompting many nations to increase their defense spending. Additionally, they have led to heightened geopolitical tensions, trade sanctions, and have contributed to rising inflation across much of the global economy. Yet, remarkably, the global economy has shown resilience and adapted to these calamities. For instance, while these two regions account for approximately 40% of the world’s energy production, oil prices are below $70 per barrel today, the lowest level since early 2021. We all hope for these conflicts to end but note that the current impact on equity investments has been limited. We are wary of significant risks if conflicts escalate and conditions deteriorate further.

The upcoming U.S. elections introduce another layer of uncertainty for the market. Over the past quarter, the stock market has shown no clear preference between the two presidential candidates, reaching record highs on days when each candidate led in national polls. Since 1950, markets have typically performed better during periods of split government: when one party controls the presidency and a different party controls at least one house of Congress. Investors seem to favor the stability of gridlock. A sweep by one party, controlling both the presidency and Congress, could unsettle the market, as investors postulate about how policies might change and ponder how such changes could affect fortunes.

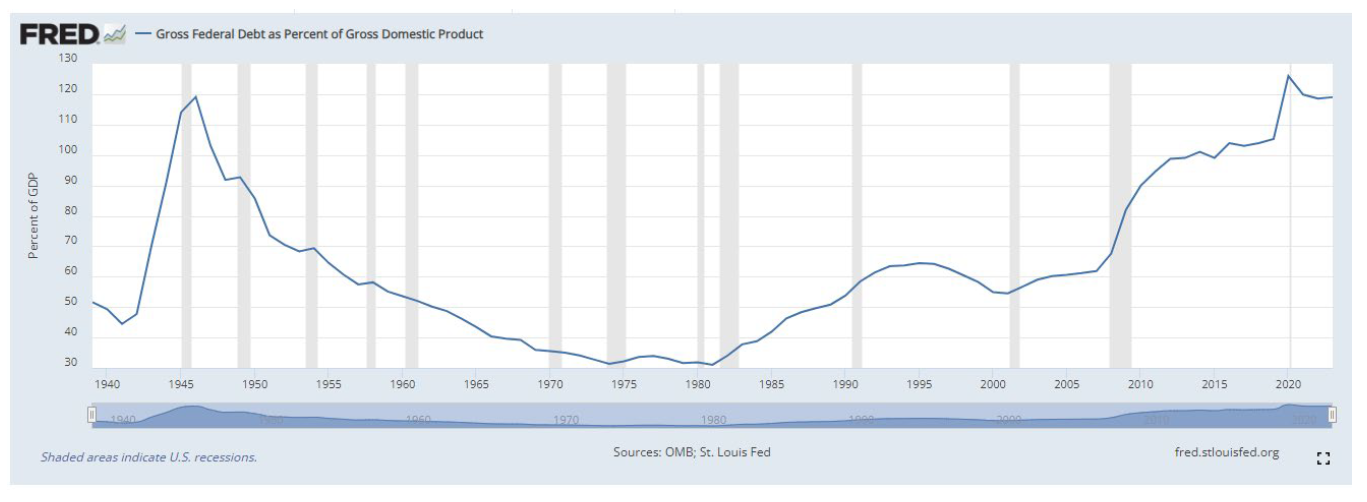

Despite the significant differences between Harris and Trump, both have centered their economic plans on tax cuts and increased spending, while ignoring the huge federal budget deficit. Both political parties are responsible for the accumulation of the record national debt, having failed to take any significant steps to reduce spending, raise revenues, or address the funding challenges facing Social Security and Medicare. The following graph shows the steady growth of the national debt as a percentage of U.S. GDP. The federal debt is currently at 120% of U.S. GDP, a level comparable to the period following World War II when the government financed extensive defense spending.

A large national debt-to-GDP ratio strains the federal budget by diverting more revenue toward interest payments, thereby reducing funds for essential services and investments. It also heightens the risk of fiscal crisis if interest rates increase. Excessive federal debt limits the government’s ability to respond to emergencies and raises concerns about long-term financial stability. And, it places a heavy repayment burden on future generations, who may need to decide between austerity or higher taxes. While markets are not currently alarmed, this is a serious concern for the U.S.

During the second quarter of 2024, the yield on the 10-year Treasury note decreased from 4.34% to 3.80%, contributing to a strong performance in the bond market. The Bloomberg Aggregate Bond Index posted total returns of 5.2% for the quarter. This decline in yield on the 10-year note represents a notable drop from last October’s 16-year high of 4.99%, reflecting the bond market’s expectation that long-term inflation will remain below 3%. To mitigate interest rate risk and capitalize on the attractive yields of shorter-term securities, we continue to maintain a relatively short average maturity for fixed-income investments in our managed portfolios.

Looking ahead, lower interest rates should continue to provide a tailwind for equity markets, stimulating the economy by reducing borrowing costs. The pace of future rate cuts by the Fed will depend on continued progress in lowering inflation and the overall health of the labor market. While the economy is expected to produce modest growth in the near term and corporate earnings are expected to expand, risks remain. A market correction would not be surprising given this year’s strong performance and the level of overvaluation in some sectors, but we remain confident that a well-diversified portfolio will offer attractive long-term returns in the face of those risks.

John D. Frankola, CFA Lawrence E. Eakin, Jr. Matthew J. Viverette Dylan C. T. Dunlop

Vista Investment Management, LLC is a Registered Investment Advisory firm. Under no circumstances does this article represent a recommendation to buy or sell stocks. This article is intended to provide information and analysis regarding investments and is not a solicitation of any kind. References to historical market data are intended for informational purposes; past performance cannot be considered a guarantee of future performance. Neither the author nor Vista Investment Management, LLC has undertaken any responsibility to update any portion of this article in response to events which may transpire subsequent to its original publication date.